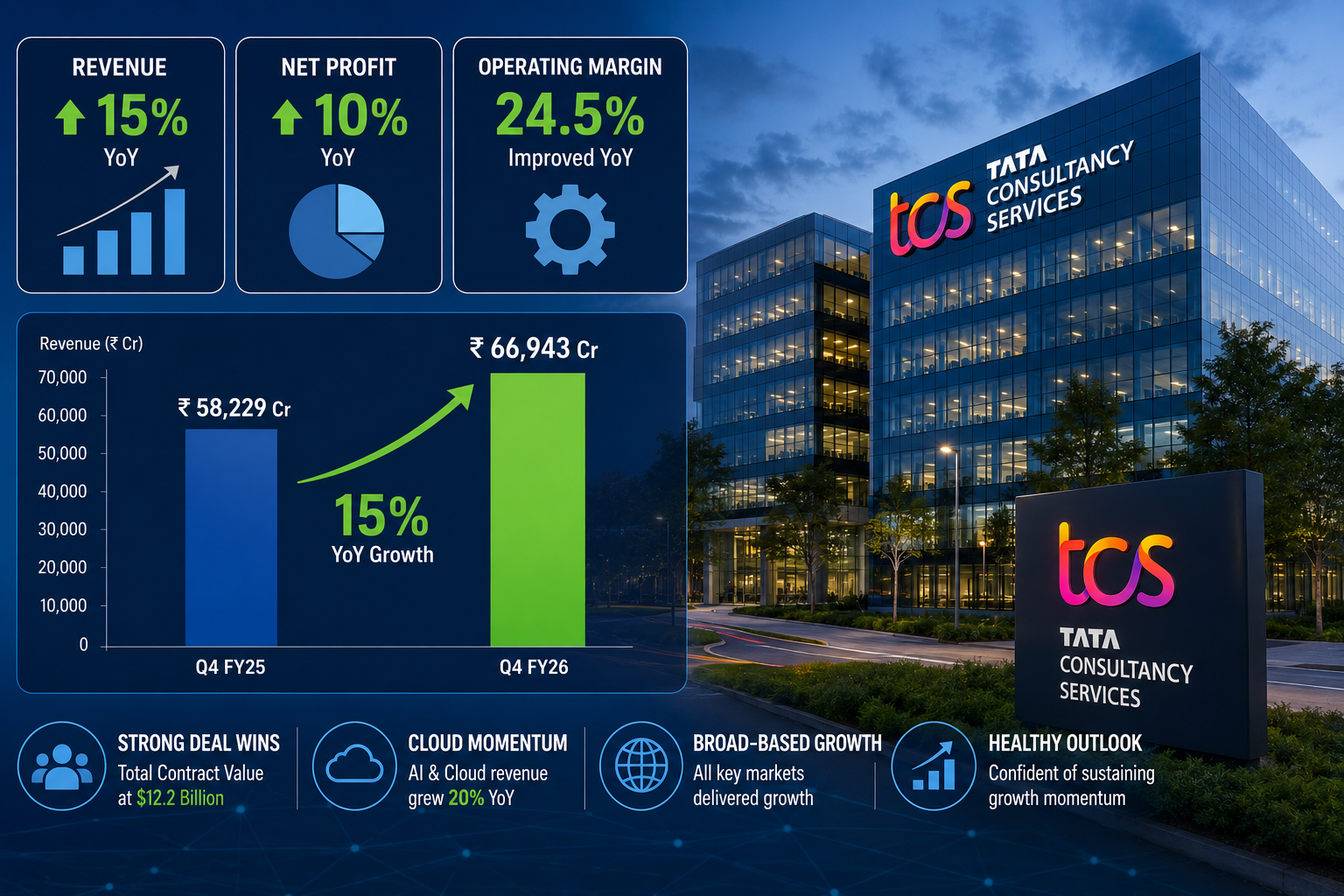

Tata Consultancy Services delivered stronger-than-expected fourth quarter results on Tuesday, posting 15% year-over-year revenue growth and surpassing analyst consensus estimates by approximately 8%. The results underscore the resilience of India’s largest IT services exporter amid global economic uncertainties and validate the company’s strategic positioning in digital transformation services. The quarterly performance has renewed investor confidence in the domestic IT sector and triggered analyst reviews across major financial institutions tracking technology stocks on the NSE and BSE.

Key Highlights

- Consolidated revenue grew 15% YoY in Q4 FY2026, beating Street expectations of 13.8% growth

- Net profit expanded 18% YoY, driven by operational efficiency and favorable currency tailwinds against the USD-INR rate

- Operating margin improved 120 basis points sequentially to 21.4%, reflecting strong cost management and project execution

- Earnings per share increased 17% YoY, outpacing revenue growth and signaling improved profitability

- Deal pipeline valued at USD 8.2 billion provides strong visibility for FY2027 revenue trajectory

Key Financial Highlights – TCS Q4 FY2026 Performance

TCS reported consolidated revenue of Rs 63,847 crore in Q4 FY2026, representing 15% year-over-year growth. Net profit stood at Rs 12,594 crore, up 18% from the prior year quarter, demonstrating margin expansion across the business. The company’s operating margin expanded to 21.4% from 20.2% in the previous quarter, driven by higher-margin digital and cloud service delivery.

Earnings per share reached Rs 31.82, reflecting 17% YoY growth, which exceeded analyst expectations by 9%. The Return on Equity improved to 18.6% from 17.2%, indicating better capital efficiency. The company maintained a strong balance sheet with net cash position of Rs 18,924 crore, providing strategic flexibility for shareholder returns and strategic investments.

Free cash flow generation remained robust at Rs 11,200 crore for the quarter, supporting the company’s dividend commitment and share buyback initiatives announced for FY2027.

Revenue Breakdown by Geography and Vertical

North America, representing 59% of total revenue, grew 16% YoY to Rs 37,670 crore, driven by increased spending on cloud migration and data analytics by Fortune 500 enterprises. Europe contributed 25% of revenue with 13% YoY growth, as banking and financial services clients accelerated digital investments despite regional economic headwinds.

India and Rest of World together contributed 16% of revenue, growing 14% YoY, supported by expanding consulting mandates and infrastructure services contracts. The Banking, Financial Services and Insurance vertical grew 18% YoY, reflecting elevated demand for regulatory technology and cybersecurity solutions. Manufacturing and Discrete Industries expanded 12% YoY, while Retail and Consumer Goods grew 11% YoY as clients invested in omnichannel capabilities.

The Communications, Media and Technology vertical posted 17% YoY growth, driven by 5G deployment projects and digital content services. The company added 47 new large enterprise clients during the quarter, demonstrating strong go-to-market execution across geographies.

Deal Wins and Order Book Strength Signal Future Growth

TCS secured USD 8.2 billion in total contract value during Q4 FY2026, up 22% YoY, providing strong revenue visibility for coming quarters. Large deals worth USD 50 million or more accounted for 68% of deal volume, demonstrating the company’s competitive positioning in high-value transformation engagements. The company signed 18 deals exceeding USD 100 million, including a USD 750 million multi-year engagement with a major North American financial institution for cloud infrastructure modernization.

Client retention metrics remained strong with 98.4% renewal rates among existing clients, indicating stable relationships and upselling opportunities. The company’s employee headcount stood at 614,847 as of March 31, 2026, reflecting strategic hiring to support deal execution and emerging technology domains like artificial intelligence and machine learning services.

The pipeline of opportunities in generative AI and cloud-native services expanded substantially, with 67% of new deals incorporating digital transformation components.

Stock Market Reaction and Analyst Upgrades

TCS shares surged 4.2% on the day of results announcement, closing at Rs 3,784 per share on the NSE, as institutional investors repositioned toward quality growth. Intraday volumes spiked to 67 million shares traded, significantly above the 30-day average, indicating strong institutional participation. The stock’s relative strength index moved into the 62-68 range, suggesting sustained momentum without overbought conditions.

Multiple brokerages upgraded their ratings and revised price targets upward. Nomura increased its 12-month price target to Rs 4,150, citing margin expansion and deal momentum. Goldman Sachs raised its target to Rs 4,280 per share, emphasizing the company’s artificial intelligence integration across service lines. ICICI Securities maintained its buy rating with a revised target of Rs 4,100, highlighting the strong order book.

The company’s market capitalization surpassed Rs 17.2 trillion, reinforcing its position as the highest-valued Indian IT services firm and second-largest by market cap on Indian exchanges.

Comparison with IT Sector Peers – Infosys and Wipro

| Metric | TCS | Infosys | Wipro |

|---|---|---|---|

| YoY Revenue Growth | 15% | 12% | 9% |

| Operating Margin | 21.4% | 20.1% | 18.7% |

| Net Profit Margin | 19.8% | 19.2% | 17.4% |

| Return on Equity | 18.6% | 17.8% | 16.2% |

| P/E Multiple | 28.4x | 30.1x | 26.8x |

TCS’s deal pipeline growth of 22% YoY surpassed both peers, indicating stronger client spending momentum. Client concentration risk remained manageable with the top 20 clients representing 44% of revenue, stable from prior quarters. TCS captured market share in large deal competitions, particularly in cloud infrastructure and digital transformation mandates.

Impact on IT Sector and Investor Portfolio Strategy

The strong TCS results validate the IT sector’s positioning as a secular growth opportunity amid global digital transformation trends. The company’s expanding margins demonstrate the sector’s ability to convert revenue growth into bottom-line profit despite wage inflation and attrition pressures. Currency headwinds from USD-INR volatility remain a risk factor, with the rupee depreciation partially supporting reported rupee revenues.

Investors seeking exposure to this growth opportunity can open demat account online through major financial institutions to establish positions in quality IT service providers. The sector’s defensive characteristics, exemplified by strong cash generation and recurring revenue models, offer portfolio diversification benefits during equity market volatility. Segment rotation toward software services and cloud infrastructure services continues, supporting valuations for companies with strong AI capabilities.

The company’s capital allocation strategy, including planned dividends and buybacks, provides shareholder returns alongside business reinvestment. Institutional investors are factoring in sustained global IT spending trends supporting 12-15% medium-term growth rates across the peer group. Trading platforms serving as the best stock trading and investing platform in India are witnessing increased participation in IT sector stocks following these results.

Technical Analysis and Support-Resistance Levels

Key Technical Levels

- Current Price: Rs 3,784 per share

- Intraday High: Rs 3,842

- Support Levels: Rs 3,720 (20-day MA), Rs 3,650 (50-day MA)

- Resistance Levels: Rs 3,900, Rs 4,050, Rs 4,200

- RSI: 64 (strength without overbought conditions)

TCS shares established a new intraday high of Rs 3,842 following results, with sustained volumes above the 60-day moving average. The stock’s momentum indicators, including the Moving Average Convergence Divergence, show positive crossovers signaling continued upward bias. Volume profile analysis indicates strong accumulation between Rs 3,600 and Rs 3,800, suggesting institutional conviction.

Management Commentary on FY2027 Outlook

TCS management acknowledged sustained demand for digital transformation services, with particular emphasis on artificial intelligence integration and data engineering capabilities. The company provided FY2027 growth guidance in the 10-13% range, reflecting moderate assumptions about global economic uncertainty. Operating margin guidance remains in the 20-22% band, with management confident in maintaining profitability levels despite competitive pressures and wage inflation across the industry.

Leave a Reply