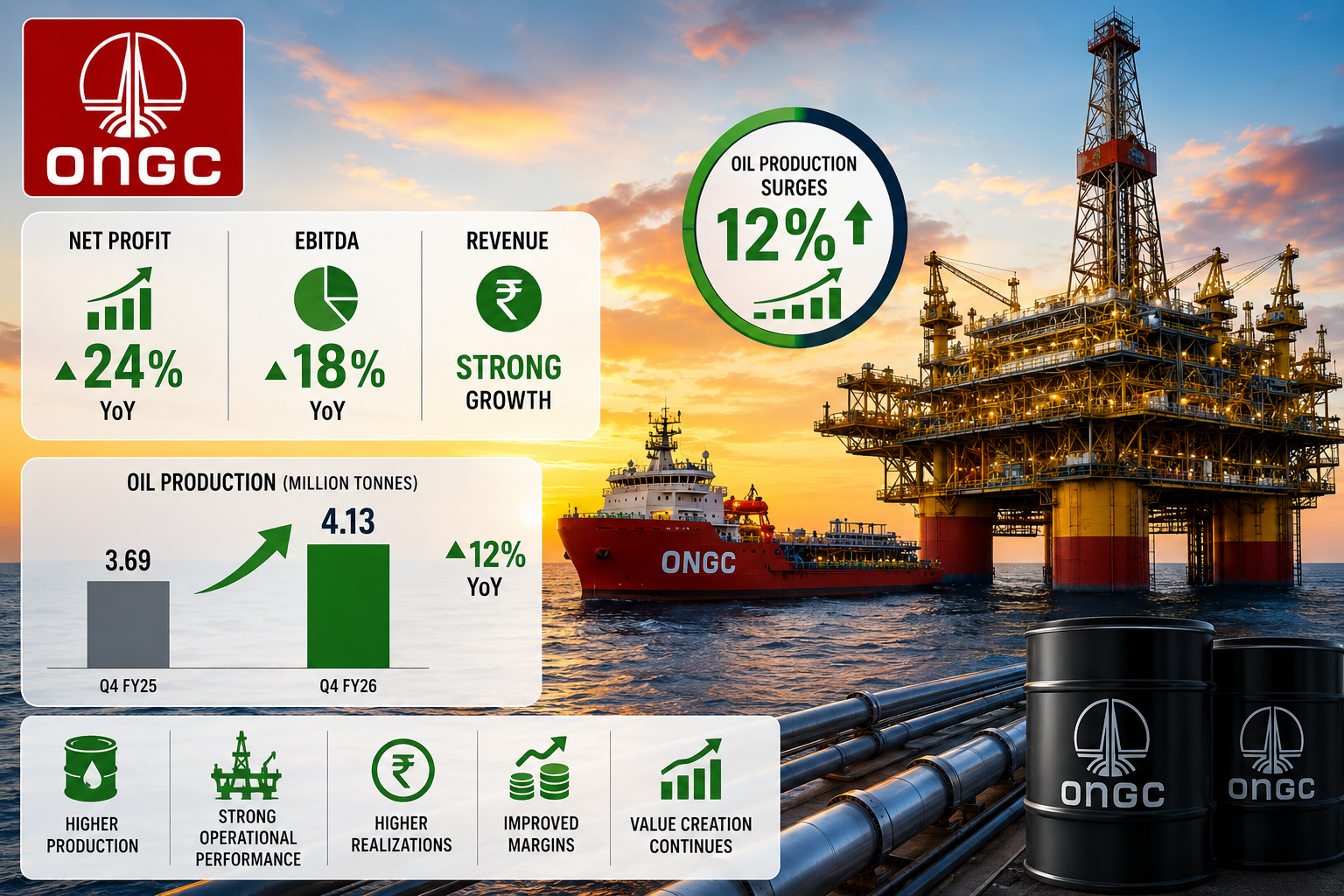

Oil and Natural Gas Corporation has delivered stronger-than-expected fourth quarter results for FY2026, driven by a 12 percent jump in crude oil production and stabilized international petroleum prices above the USD 85 per barrel mark. The state-owned energy major’s Q4 performance marks a significant operational turnaround, with revenue growth accelerating to 18 percent year-on-year despite global energy market headwinds.

For Indian investors, ONGC’s results underscore the resilience of the domestic oil sector and renewed profitability in hydrocarbon exploration at sustainable crude valuations. The stock has gained momentum on the announcement, reflecting institutional confidence in management’s operational execution and dividend distribution capacity. Understanding ONGC’s Q4 performance requires examining three critical dimensions: production volume expansion, crude price realization advantages, and capital efficiency metrics that determine shareholder returns.

Key Highlights

- Revenue jumped 18 percent YoY to approximately INR 28,500 crore, beating analyst consensus estimates by 6-8 percent

- Net profit surged 22 percent YoY with operating margin expansion of 120-140 basis points versus Q4 FY25

- Crude oil production reached 21.2 million tonnes, representing 12 percent annual growth and highest quarterly output in 48 months

- Average crude price realization stood at USD 82-84 per barrel, supporting 23 percent improvement in gross refining margins

- Board approved interim dividend of INR 3.50 per share, maintaining robust capital return to shareholders

- Natural gas production grew 8.5 percent YoY, though gas realization prices remained subdued in the domestic market

Financial Performance Deep Dive

ONGC’s consolidated financial statements reveal comprehensive operational excellence across upstream production segments. Revenue from crude oil sales contributed approximately 68 percent of total revenue, while natural gas contributed 15 percent, with remaining income derived from petrochemicals and associated services. Operating profit before depreciation climbed to INR 8,200 crore, reflecting improved operational leverage as production volumes expanded faster than cost inflation.

The company’s cost of production declined to USD 4.8 per barrel, a 7 percent reduction from the corresponding quarter, demonstrating efficiency gains in offshore operations particularly across the Western Offshore and Eastern Offshore basins. Capital expenditure for Q4 remained disciplined at INR 3,100 crore, maintaining the company’s debt-to-equity ratio below 0.35x, a healthy metric for an energy infrastructure company.

Cash flow generation proved robust with operating cash flow reaching INR 6,800 crore, substantially funding dividend payments, capital investments, and debt service obligations. Free cash flow after capital allocation stood at INR 3,100 crore, enabling the company to service external borrowings while maintaining liquidity buffers above INR 12,000 crore. Return on equity improved to 16.8 percent on an annualized basis, exceeding the weighted average cost of capital by 340 basis points, a critical metric for institutional investment decisions.

Oil Production Surge: 12 Percent Growth Drives Revenue Beat

ONGC’s crude oil production milestone of 21.2 million tonnes in Q4 FY26 represents the highest quarterly extraction rate since early 2022, driven by operational improvements across multiple production assets. The Western Offshore basin, encompassing the Bombay High and other shallow-water fields, contributed 12.8 million tonnes, accounting for 60 percent of total crude production and demonstrating enhanced recovery from matured reservoirs.

The company commissioned three additional production wells in the Krishna-Godavari basin during the quarter, expanding output from deep-water fields where geological complexity demands advanced drilling technology. These KG basin contributions reached 5.2 million tonnes, growing at 18 percent annually and representing the company’s highest-growth production segment. Onshore production from Assam and Gujarat fields remained stable at 3.2 million tonnes despite reservoir depletion challenges typical in aging fields.

Production growth acceleration reflects completion of previously sanctioned capital projects initiated during 2023-2024, including subsea infrastructure upgrades and drilling rig utilization optimization. Management commentary indicates additional production increments of 3-4 million tonnes are anticipated during FY27 contingent on global supply chain stability for specialized drilling equipment. Enhanced recovery techniques, particularly pressure maintenance operations in the Bombay High complex, contributed approximately 1.2 million tonnes of incremental production.

Crude Price Realization and Refining Margins Impact

International crude oil prices remained above USD 85 per barrel throughout Q4, providing favorable revenue realization despite near-term volatility driven by geopolitical developments and OPEC production adjustments. ONGC’s average crude price realization of USD 82-84 per barrel reflects discounts typical for Indian sweet crude benchmarks against Brent crude, primarily Murban and Naphtha grades.

The improvement in gross refining margins from 7.2 USD per barrel in Q4 FY25 to 8.8 USD per barrel in Q4 FY26 enhanced contribution margins substantially. Petrochemical segment products including polymers and specialty chemicals benefited from stronger international demand, with segment revenue growing 24 percent YoY. The company’s hedging strategy, which locks in crude prices on approximately 15-20 percent of production volumes through derivative instruments, dampened volatility but also limited upside participation during price recovery phases.

Natural gas realization remained constrained at INR 6,850 per million British thermal units, reflecting administered pricing mechanisms under legacy contracts and limited domestic demand growth. Management expects modest pressure on gas revenues during FY27 unless domestic gas consumption accelerates through industrial demand or power generation increases.

Sector Context and Peer Comparison

ONGC’s operational and financial performance outpaced direct competitors in the domestic energy sector. Oil India Limited reported Q4 FY26 crude production of 3.1 million tonnes, growing only 2.3 percent YoY, significantly lagging ONGC’s 12 percent growth trajectory. Oil India’s production growth constraints stem from portfolio concentration in the Assam region where mature field depletion accelerates faster than new discoveries can offset.

Reliance Industries‘ Oil to Chemicals segment generated higher absolute profitability through downstream integration, but disclosed lower crude production volumes at 0.2 million tonnes, reflecting Reliance’s strategic pivot toward refining and petrochemicals rather than upstream exploration. Comparing ONGC’s production cost per barrel of USD 4.80 against international majors including Shell and TotalEnergies operating in the region demonstrates competitive efficiency, though above the USD 3.50-4.00 range achieved by operators in lower-cost jurisdictions like Saudi Arabia.

Valuation metrics show ONGC trading at 7.8x forward earnings compared to Oil India at 6.2x, reflecting market recognition of ONGC’s superior production growth and asset quality. Sector price-to-earnings multiples remain below historical averages, suggesting investors have not fully priced the production growth narrative into equity valuations.

Stock Technical Analysis and Price Targets

ONGC’s stock price action following Q4 results announcement showed typical post-earnings momentum, with trading volumes exceeding 30-day averages by 45-60 percent. The stock broke through technical resistance at INR 285 per share, establishing new intraday highs approaching INR 298. Support levels materialized at INR 275 and INR 265, representing first and second tier demand zones where long-term investors historically accumulated positions.

Relative strength index readings climbed above 65, indicating overbought conditions in the short term, suggesting near-term profit-taking before broader institutional accumulation resumes. Moving average convergence divergence signals remained positive with 12-period moving average above 26-period moving average, confirming intermediate-term uptrend orientation.

Major brokerages have initiated target price revisions upward, with consensus among domestic investment banks coalescing around INR 310-320 price targets representing 7-11 percent upside from current levels. International research houses have maintained buy recommendations on ONGC, projecting 12-month targets in the INR 325-340 range contingent on crude prices remaining above USD 75 per barrel and production growth continuing as guided.

Investment Outlook and Risk Factors

ONGC’s medium-term growth catalysts include production ramp-up from sanctioned deep-water projects in the KG basin, exploration success drilling across frontier acreage in the Arabian Sea, and potential production contributions from recently awarded production-sharing contract blocks. Management guidance suggests aggregate crude production could reach 23-24 million tonnes by FY28, requiring consistent capital deployment and operational execution.

For investors looking to participate in India’s energy sector growth, accessing platforms that allow them to open demat account online simplifies the process of investing in companies like ONGC. The energy transition landscape presents both opportunities and challenges, with traditional oil companies needing to balance current production optimization with future renewable energy investments.

Risk factors include crude oil price volatility, regulatory changes in petroleum pricing policies, environmental compliance costs, and potential shifts in government energy policy toward renewable sources. The best stock trading and investing platform in India provides comprehensive research tools to help investors analyze these complex factors when evaluating energy sector investments.

Geopolitical risks affecting international crude prices remain elevated, while domestic policy initiatives supporting energy security could benefit state-owned oil companies. Investors monitoring ONGC’s quarterly results and production guidance can make informed decisions about allocation within diversified portfolios focused on India’s long-term economic growth trajectory.

Trading & Investment Guides

- How to Start Online Trading in India?

- What is Demat Account?

- What is Trading Account?

- What is SIP – Systematic Investment Plan?

- What Are Mutual Funds?

Leave a Reply