India’s infrastructure ambitions are massive, and steel is the backbone of that growth. While many investors focus on steel manufacturers, smart retail investors often look upstream to the raw materials that make steel production possible. This brings us to the upcoming initial public offering (IPO) of Bharat Coking Coal Limited (BCCL). As a subsidiary of the state-owned giant Coal India Limited, BCCL holds a unique and dominant position in the energy sector.

Scheduled to open for subscription in January 2026, this IPO represents a significant opportunity for the public to own a stake in India’s largest producer of coking coal. But is this public sector undertaking (PSU) a solid addition to your portfolio? To help you make an informed decision, we are breaking down the company’s business model, analyzing its financial health, and evaluating the long-term growth prospects.

IPO Snapshot: Key Dates and Details

Before analyzing the fundamentals, let’s look at the logistical details of the offer. The IPO is structured entirely as an Offer for Sale (OFS), meaning the promoter, Coal India Limited, is selling a portion of its stake to the public. BCCL itself will not receive proceeds from this issue.

Here are the essential details you need to mark on your calendar:

- IPO Open Date: January 9, 2026

- IPO Close Date: January 13, 2026

- Price Band: ₹21 to ₹23 per share

- Lot Size: 600 Shares

- Total Issue Size: ₹1,071 Crore

- Tentative Listing Date: January 16, 2026

- Listing Exchanges: BSE and NSE

For retail investors, the entry point is accessible, with the price band set between ₹21 and ₹23, and interested investors can apply now during the offer period to participate in the listing.

Company Overview: The Coking Coal Monopoly

To understand the value of BCCL, you must understand the difference between thermal coal and coking coal. While thermal coal is used to generate electricity, coking coal is an irreplaceable ingredient in steel manufacturing.These fundamentals form the basis of the Bharat Coking Coal Ltd. IPO details for investors evaluating the company.

Bharat Coking Coal Limited is the undisputed leader in this space. As of FY25, the company accounted for 58.50% of domestic coking coal production. More importantly, BCCL is the only source of prime coking coal in India. This gives the company a significant competitive moat.

Operational Footprint

BCCL operates primarily in the Jharia coalfield in Jharkhand and the Raniganj coalfield in West Bengal. These are historic mining zones with rich deposits. The company currently manages:

- 34 Operational Mines: A mix of opencast, underground, and mixed projects.

- 5 Operational Washeries: Located at Moonidih, Madhuband, Dahibari, Patherdih I, and Madhuband NLW.

The company is also backed by a massive resource base of approximately 7.91 billion tonnes, providing high visibility for long-term production.

Revenue Model

BCCL generates revenue through three main channels:

- Raw Coal: Sales of coking coal to steel plants and non-coking coal to power plants.

- Washed Coal: Coal that has been processed to reduce ash content, fetching a higher price.

- By-products: Sales of middlings, slurry, and rejects.

The clientele is impressive, consisting largely of Public Sector Undertakings (PSUs) and major power producers like SAIL, NTPC, and Damodar Valley Corporation.

Industry Landscape: The Demand for Steel

The investment case for BCCL is closely tied to India’s steel industry. The government has set an ambitious target to reach a crude steel capacity of 300 million tonnes per annum (MTPA) by FY31. Since coking coal is a non-substitutable input for steel, demand is expected to remain robust.

Currently, India imports about 90% of its coking coal requirements, mostly from Australia and the USA. This high import dependence is a strategic vulnerability for the country. Under the “Atma-Nirbhar Bharat” (Self-Reliant India) initiative, the government is pushing hard for import substitution.

This is where BCCL plays a critical role. By expanding its production and washing capabilities, BCCL aims to replace expensive imported coal with domestic supply. This macro-economic tailwind provides a long runway for growth.

Financial Analysis: A Deep Dive

For a retail investor, the numbers tell the real story. Let’s analyze BCCL’s financial performance over the last few years to gauge its stability and profitability.

Revenue Trends

BCCL has shown consistent sales performance.

- FY23 Sales: ₹132,809 Million

- FY24 Sales: ₹140,453 Million

- FY25 Sales: ₹139,984 Million

While sales were relatively flat in FY25, projections for the future are optimistic. Revenue is forecast to grow to ₹153,798 Million in FY26 and ₹172,995 Million in FY27. This growth is expected to be driven by increased production volumes and better realization per tonne.

Profitability and Margins

The company has seen a significant improvement in its operating margins.

- EBITDA Margin: Jumped from 4% in FY23 to 15% in FY24, stabilising at 13% in FY25.

- Net Profit: Rose from ₹6,647 Million in FY23 to ₹12,401 Million in FY25.

It is worth noting that FY25 saw a dip in profit compared to FY24 (which was ₹15,644 Million). This was largely due to external headwinds, including excessive rainfall that hampered production and offtake. However, cost efficiency measures helped mitigate the impact.

Balance Sheet Strength

One of the most attractive features of BCCL for a risk-averse retail investor is its debt-free balance sheet. The company has no long-term borrowings and has successfully eliminated accumulated losses as of FY24. This financial resilience allows the company to invest in modernization without the burden of high interest payments.

Key Ratios

- Return on Net Worth (RoNW): Stood at 20.83% in FY25, indicating efficient use of shareholder equity.

- Return on Capital Employed (ROCE): A healthy 30.13% in FY25, showing strong returns on the capital invested in the business.

- Earnings Per Share (EPS): ₹2.7 in FY25, projected to rise to ₹3.3 in FY26 and ₹3.7 in FY27.

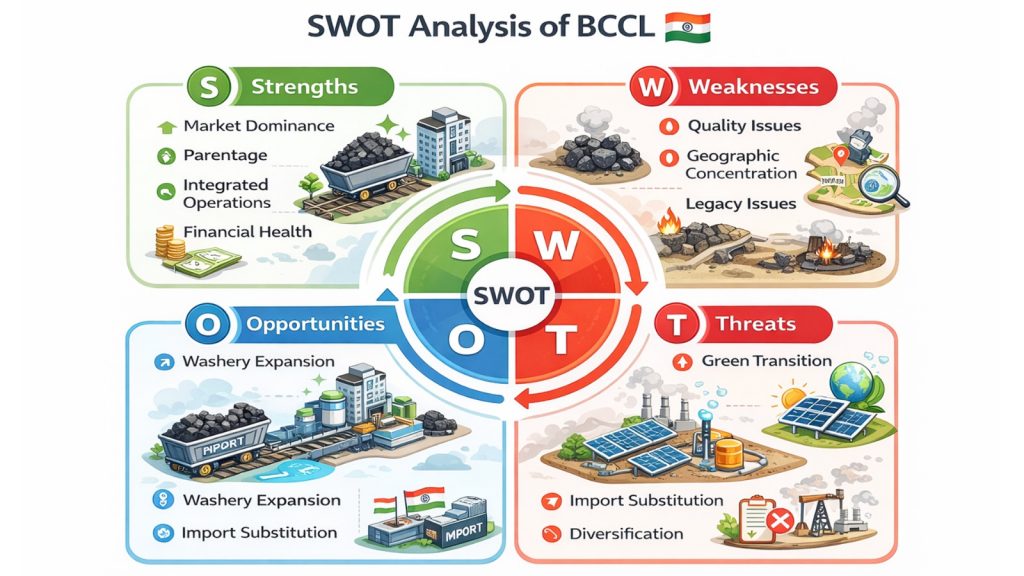

SWOT Analysis

Every investment carries risks and rewards. Here is a breakdown of BCCL’s position:

Strengths

- Market Dominance: Largest producer of coking coal in India.

- Parentage: Backed by Coal India Limited, ensuring financial and technical support.

- Integrated Operations: Strong rail and road connectivity in mining zones.

- Financial Health: Zero long-term debt and strong cash flow generation potential.

Weaknesses

- Quality Issues: Domestic coal has high ash content, requiring washing/beneficiation before it can be used in steel production.

- Geographic Concentration: Operations are concentrated in Jharia and Raniganj, making the company vulnerable to regional disruptions.

- Legacy Issues: The Jharia coalfield faces environmental challenges, including underground mine fires and land subsidence.

Opportunities

- Washery Expansion: BCCL is adding 7.00 MTPA of new washery capacity. This will improve the quality of coal, making it more competitive against imports.

- Import Substitution: As steel demand rises, domestic steelmakers are eager to source local coal to reduce costs.

- Diversification: The company is expanding into Coal Bed Methane (CBM) and solar power, opening new revenue streams.

Threats

- Green Transition: The long-term global shift toward renewable energy and India’s net-zero 2070 target poses a structural risk to the coal industry.

- Regulatory Changes: Stricter environmental norms could increase compliance costs.

Every investment carries risks and rewards. Here is a breakdown of BCCL’s position:

Strengths

- Market Dominance: Largest producer of coking coal in India.

- Parentage: Backed by Coal India Limited, ensuring financial and technical support.

- Integrated Operations: Strong rail and road connectivity in mining zones.

- Financial Health: Zero long-term debt and strong cash flow generation potential.

Weaknesses

- Quality Issues: Domestic coal has high ash content, requiring washing/beneficiation before it can be used in steel production.

- Geographic Concentration: Operations are concentrated in Jharia and Raniganj, making the company vulnerable to regional disruptions.

- Legacy Issues: The Jharia coalfield faces environmental challenges, including underground mine fires and land subsidence.

Opportunities

- Washery Expansion: BCCL is adding 7.00 MTPA of new washery capacity. This will improve the quality of coal, making it more competitive against imports.

- Import Substitution: As steel demand rises, domestic steelmakers are eager to source local coal to reduce costs.

- Diversification: The company is expanding into Coal Bed Methane (CBM) and solar power, opening new revenue streams.

Threats

- Green Transition: The long-term global shift toward renewable energy and India’s net-zero 2070 target poses a structural risk to the coal industry.

- Regulatory Changes: Stricter environmental norms could increase compliance costs.

Yes, BCCL is a wholly-owned subsidiary of Coal India Limited, which is a Maharatna PSU under the Ministry of Coal, Government of India.

Thermal coal is burned to create steam for electricity generation. Coking coal (metallurgical coal) is baked in a furnace to create coke, which is used to smelt iron ore into steel. BCCL specializes in coking coal.

This IPO is an Offer for Sale (OFS). This means existing shares held by the promoter (Coal India) are being sold to the public. The money goes to the promoter, not the company’s treasury.

The minimum investment for a retail investor is one lot. With a lot size of 600 shares and a price band of ₹21-₹23, the minimum investment would be between ₹12,600 and ₹13,800.

No, as of the latest financial reports, BCCL has a debt-free balance sheet with no long-term borrowings.

Disclaimer: This blog is intended solely for educational and informational purposes and should not be construed as investment advice or a recommendation. While efforts have been made to ensure the accuracy and reliability of the information and data presented, no representation or warranty, express or implied, is made regarding its completeness or correctness. Readers are advised to independently verify all information and consult a qualified financial advisor before making any investment decisions. Investments in the securities market are subject to market risks. Please read all relevant offer documents and disclosures carefully before investing.

Leave a Reply